世界的なサプライチェーンの再構築が進む中、カンボジアはバッグ製造の新興勢力として急速に台頭している。 ベトナムのバッグメーカー 東南アジアの製造業のベンチマークとして長らく認識されてきたカンボジアだが、最新のデータによると、旅行用品分野で独自の競争優位性を発揮していることが明らかになった。2025年には、カンボジアのバッグ輸出額は20億ドルを超え、衣料品、履物、旅行用品(GFT)産業全体の輸出額は過去最高の160億ドルに達した。

この記事では、カンボジアのバッグ工場がベトナムのバッグ工場に対して持つ5つの主要な利点を詳細に分析し、サプライチェーンに関する意思決定に役立つデータに基づいた洞察を提供します。

カンボジアの最低賃金はわずか月額210ドル(2026年基準)で、 ベトナムのバッグ工場 現在の労働コスト。カンボジア政府による年次調整(2026年の増加はわずか2ドルから210ドル)にもかかわらず、この段階的なアプローチは労働者の福祉と産業コストの競争力とのバランスを取っている。

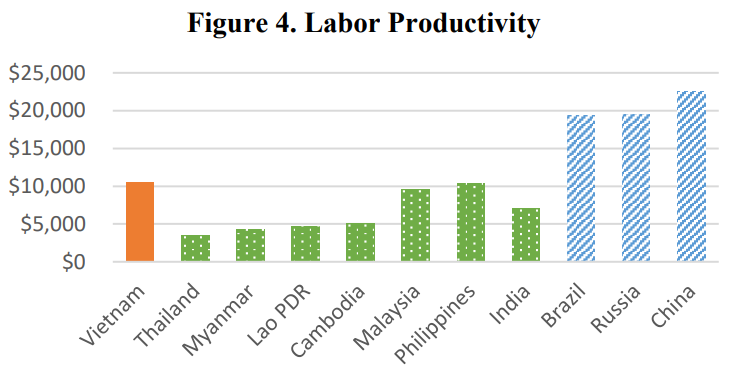

バッグのような労働集約型製品の場合、このコスト差はベトナムのバッグメーカーに対する15~20%の製造コスト優位性に直結する。特筆すべきは、カンボジアの労働生産性が着実に上昇を続けており、2019年には工業部門の生産性が労働者一人当たり2,424ドルに達したことである。

これはカンボジアにとって戦略的に最も価値のある差別化要因であり、 ベトナムのバッグメーカー。

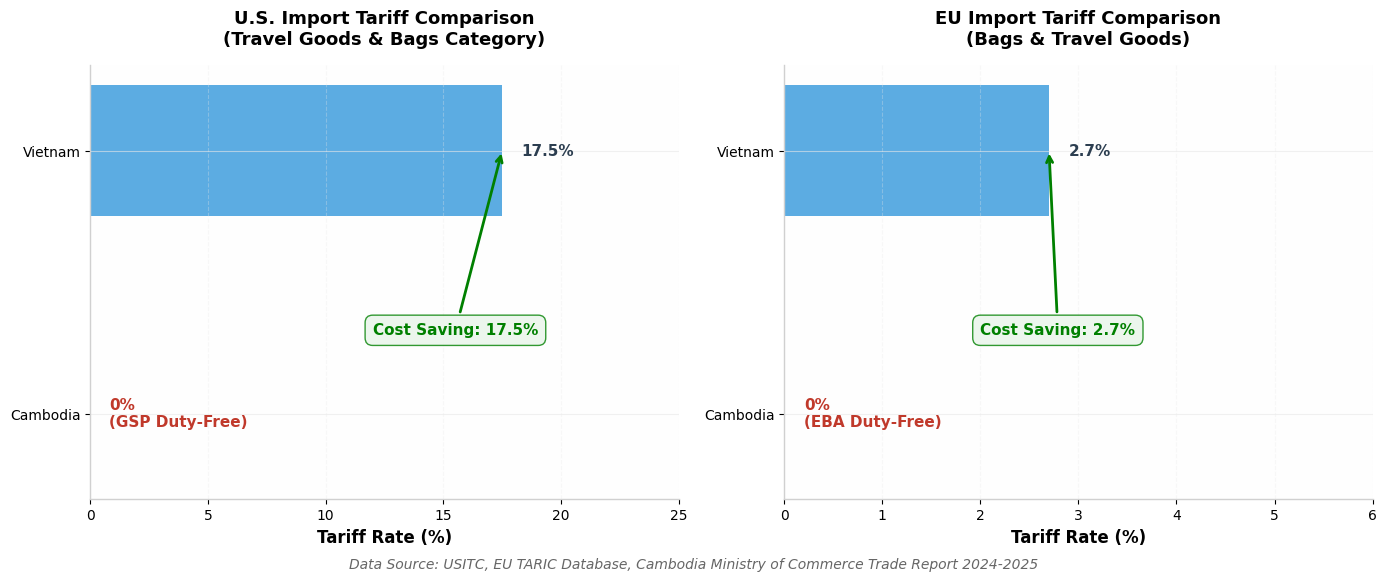

2016年以来、カンボジアは米国の一般特恵関税制度(GSP)の適用を受けており、旅行用品(スーツケース、バックパック、ハンドバッグ、財布など)を米国市場に無税で輸出することが可能となっている。一方、ベトナムのバッグ工場で生産される同様の製品には、最恵国待遇(MFN)関税として10~30%が課せられている。

2025年にカンボジアに19%の米国関税が課されたとしても、労働コストの優位性により、カンボジアのバッグ製造業はベトナムやタイのバッグ製造業と競争力を維持できる。さらに、カンボジアは以下の利点も享受できる。

これらの特恵貿易協定により、バッグ輸出業者はベトナムのバッグ工場と比較して、関税費用を12~33%削減できる。

関税コストの定量化:これは、ベトナムの工場との最も直接的なコスト競争力比較です。米国市場では、カンボジアのバッグは一般特恵関税制度(GSP)により関税が0%ですが、ベトナムのバッグ工場製品は平均17.5%の最恵国待遇関税(10~30%)に直面しています。

EU市場も同様に有利だ。EBA(武器以外の全品目)の適用により、カンボジアはEU市場で関税ゼロの恩恵を受けている一方、ベトナムのバッグ製造業者はEVFTA(欧州連合・ベトナム自由貿易協定)の恩恵を受けているにもかかわらず、平均2.7%の関税を支払っている。利益率の低いバッグ業界にとって、この2.7%の差は規模が大きくなると大きな意味を持つ。

リスクに関する注記:米国の一般特恵関税制度(GSP)には不確実性(過去に断続的に実施されてきた)が伴いますが、カンボジアのバッグ製造業は、労働コストの優位性により、2025年の関税率19%シナリオにおいても、ベトナムのバッグ工場と全体的なコスト競争力を維持しています。さらに、EUのEBA(欧州総合武器免除)の恩恵は少なくとも2029年まで保証されており、中長期的な計画策定に確実性をもたらします。

カンボジアは、衣料品、履物、旅行用品(GFT)に特化した産業クラスターを設立しました。2024年現在、同国には約1,600のGFT工場があり、80万人以上の労働者を雇用しており、そのうち75.5%が女性です。

ベトナムのバッグ工場が幅広い製造基盤を持っているのとは異なり、カンボジアはバッグ製造において高度に専門化された部門を発展させてきた。

カンボジアのGFT産業開発戦略2022-2027に基づき、政府は純粋なCMT(裁断・製造・仕上げ)モデルからOEM/ODM能力へのアップグレードを積極的に推進しており、カンボジアの工場は現在、ベトナムの工場に匹敵する設計開発や高付加価値の受注に対応できる能力を備えている。

ベトナムのバッグ工場は巨大工場が主流の構造であるのに対し、カンボジアの工場はより柔軟な規模で運営されており、小ロット生産、多様なスタイルへの対応、迅速な納期といった独自の利点を提供している。

データによると、カンボジアの工場における一般的な最小発注数量(MOQ)は、スタイルごとに3,000~5,000個です。SYNBERRY BAG CAMBODIAのような企業は、大手ブランドの品質と生産能力に関する要件を満たしつつ、中国での生産やベトナムの大規模工場に代わる選択肢を求める中小規模ブランド向けに、柔軟なOEM/ODM製造能力を提供することができます。

カンボジア政府は製造業を経済の柱と位置付けており、工業部門は2025年に8.6%の成長が見込まれ、2年連続で8%以上の成長を達成する見込みである。こうした政策の安定性は、長期投資に対する安全策となる。

ベトナムのバッグ製造業が貿易摩擦リスクにさらされているのに対し、カンボジアは2029年まで後発開発途上国(LDC)の地位を維持し、この緩衝期間中は特別な国際貿易上の優遇措置を受けることができる。LDC卒業後も、カンボジアは人権と環境基準を満たしていれば、GSP+プログラムを通じてEU市場への無関税アクセスを維持できる。これは、責任あるブランド価値提案と完全に合致する。

結論:カンボジア―バッグ製造における戦略的優位地(対ベトナムのサプライヤー)

コスト最適化、関税優遇、柔軟な生産能力を求めるバッグブランドにとって、カンボジアは多くのベトナムサプライヤーが再現に苦慮する魅力的な選択肢となる。特に米国市場においては、GSP(一般特恵関税制度)による無関税の恩恵(この政策が継続される場合)は、ベトナムからの輸入品に対して10~30%の価格競争力に直結する可能性がある。

公式の輸出入データは、カンボジアがベトナムのバッグ産業に対して製造面で優位性を持っていることを裏付けています。過去5年間で、カンボジアの旅行用品輸出は飛躍的な成長を遂げ、2020年の12億5000万ドルから2025年には20億ドルへと、累計で60%増加しました。一方、ベトナムは絶対的な数量では優位性(48億ドル)を維持しているものの、成長率は大幅に鈍化しており、過去5年間でわずか26%の成長にとどまっています。これは、2021年には市場が飽和状態に達しつつあることを示しています。

ベトナムの工場はインフラの高度化という点で優位性を保っているものの、労働集約型で比較的標準化されたバッグ製品(主に米国とEU市場に輸出される)に関しては、カンボジアはベトナムにおける従来の調達先と比べて、間違いなくより戦略的に将来を見据えた選択肢と言えるだろう。

したがって、サプライチェーンのレイアウトを検討しているブランドには、「中国+カンボジア」の二拠点戦略をお勧めします。つまり、高度な複雑性や柔軟性が求められる生産要件は中国で維持しつつ、標準化されたバッグ製品ラインはカンボジアに移管することで、関税上のメリットとベトナムでの製造オプションに対するコスト面での優位性を最大限に活用する戦略です。

ベトナムのバッグ工場からの既存の注文を移管することを検討している場合でも、東南アジアに初めて製造拠点を設立することを検討している場合でも、当社のチームは工場監査、サンプル開発から量産、納品まで、エンドツーエンドのサポートを提供します。

今すぐお問い合わせください:

メールアドレス:[email protected]

WhatsApp: +86-139-5921-4481

(すべてのデータソース:カンボジア商務省、ユーロチャム・カンボジア、GMAC(カンボジア衣料品製造業者協会)、アジアアパレル産業観測レポート(2024-2025年))

ぜひ読んで、投稿を続け、購読してください。ご意見をお聞かせください。

著作権

@2024 Synberry Bag & Package Products Co.,Ltd 無断転載を禁じます

.

サポートされているネットワーク

サポートされているネットワーク

サイトマップ / ブログ / Xml / プライバシーポリシー